@misc{doubleml,

title = {DoubleML},

author = {Bach and Chernozhukov and Kurz and Spindler},

howpublished = {\url{https://docs.doubleml.org/}},

note = {Software / documentation}

}When the tails matter: estimate potential quantiles and the conditional value-at-risk of a treatment with Neyman-orthogonal scores.

Input · what goes in

Outcome Y, binary treatment D, covariates X — when you care about quantiles / tail risk, not the mean.

Show data format & exampleHide example

Format — one row per unit: y, d ∈ {0,1}, covariates X.

y d x1 x2

0.4 1 0.4 -1.1

-1.1 0 -0.1 0.6

Pipeline · the recipe ⑂ has parallel branches

↑ Click any step in the diagram to read its logic, code, assumptions & discussion.

Build DoubleMLData (y, d, X)

Data preparation — shapes the raw inputs into what the estimator expects.

Declare outcome, binary treatment and covariates.

dml_data = dml.DoubleMLData(df, 'y', 'd', x_cols=X)

- No comments on this step yet — be the first.

Log in to comment on this step.

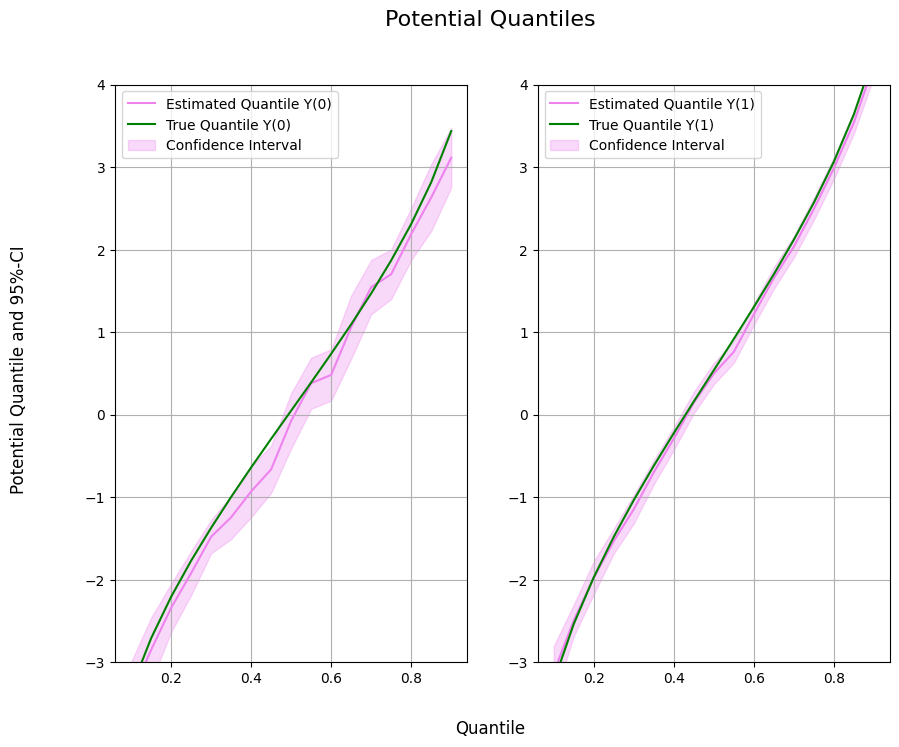

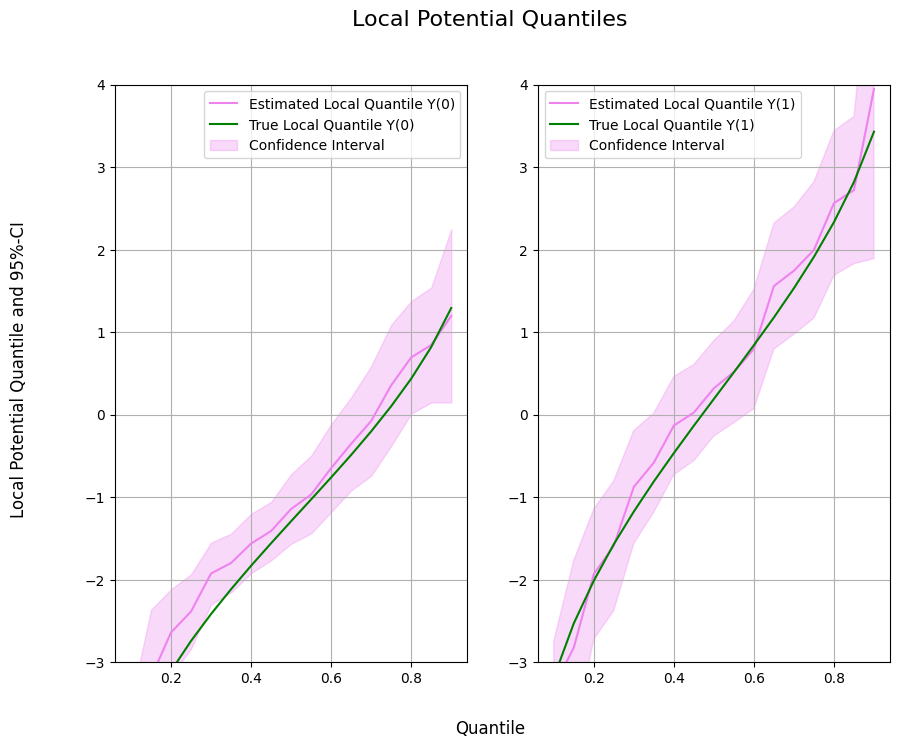

Potential quantiles

The core estimate — where the causal quantity itself is computed.

A debiased τ-quantile of each potential outcome.

pq = dml.DoubleMLPQ(dml_data, ml_g, ml_m, quantile=0.5).fit()

- No comments on this step yet — be the first.

Log in to comment on this step.

Conditional value-at-risk

The core estimate — where the causal quantity itself is computed.

Average outcome in the lower tail below the τ-quantile — orthogonally identified.

cvar = dml.DoubleMLCVAR(dml_data, ml_g, ml_m, quantile=0.1).fit()

- No comments on this step yet — be the first.

Log in to comment on this step.

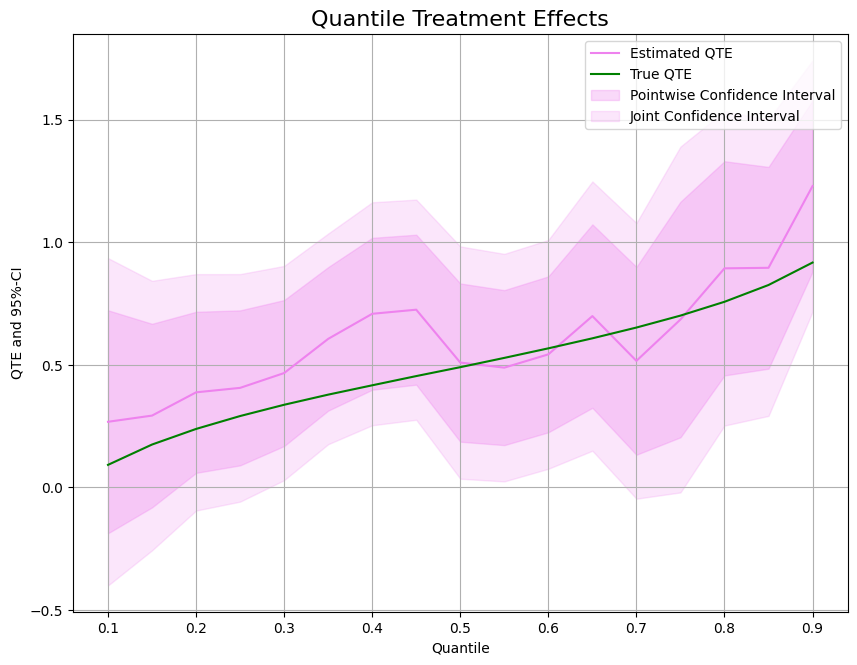

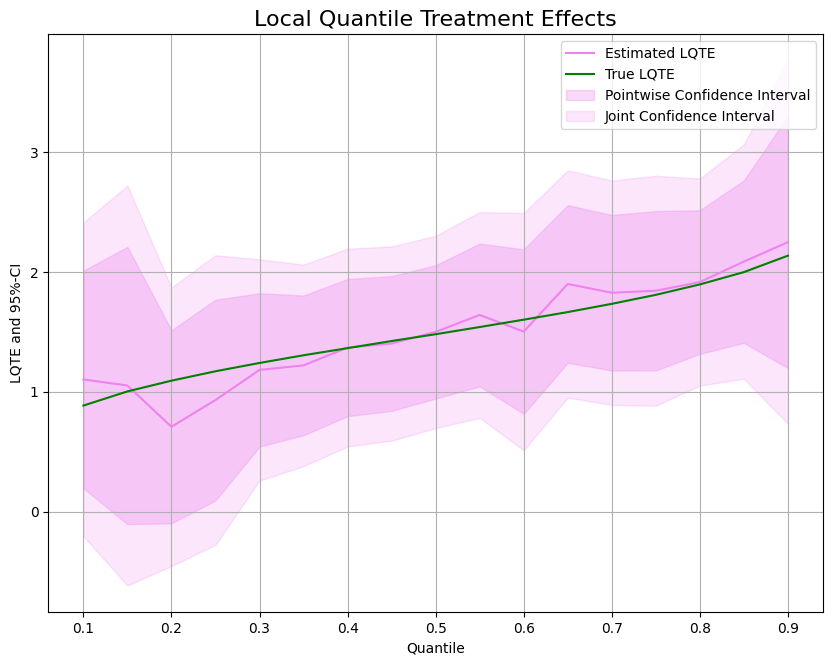

Plot quantile & CVaR effects

Reporting — turn the numbers into a figure or table a reader can act on.

Effect across the distribution and in the tail.

# quantile/CVaR effect vs tau, with CIs

- No comments on this step yet — be the first.

Log in to comment on this step.

Output · what you get 4 figures

Figures reproduced from DoubleML — Bach, Chernozhukov, Kurz & Spindler — unofficial community showcase; all credit to the original authors.

⚠️ Unofficial community showcase of a DoubleML example. Not affiliated with the authors; figures are from the public documentation. All credit to Bach, Chernozhukov, Kurz & Spindler.

When the tails matter: estimate potential quantiles and the conditional value-at-risk of a treatment with Neyman-orthogonal scores.

Discussion (0)

Log in to join the discussion.