@misc{doubleml,

title = {DoubleML},

author = {Bach and Chernozhukov and Kurz and Spindler},

howpublished = {\url{https://docs.doubleml.org/}},

note = {Software / documentation}

}Effect of 401(k) eligibility on net assets via PLR / IRM / IIVM with cross-fit ML nuisances — four learners, one honest comparison.

Input · what goes in

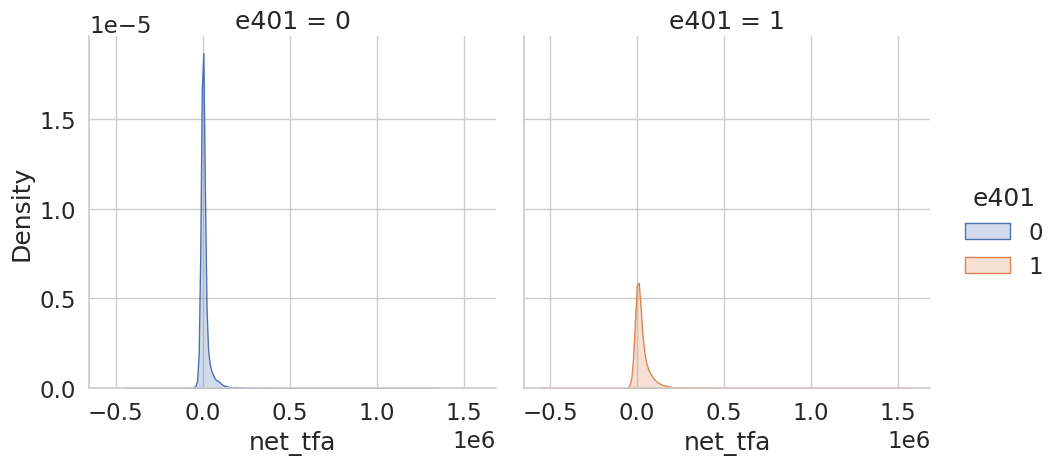

Outcome (net financial assets), treatment (401(k) eligibility), covariates, and an instrument (eligibility) for the IV model.

Show data format & exampleHide example

Format — one row per household: outcome y, treatment d, covariates X (and instrument z for IIVM).

net_tfa(y) e401(d) age inc educ ...

12000 1 41 38k 13

-400 0 53 21k 11

Pipeline · the recipe ⑂ has parallel branches

↑ Click any step in the diagram to read its logic, code, assumptions & discussion.

Build DoubleMLData (y, d, X, z)

Data preparation — shapes the raw inputs into what the estimator expects.

Declare outcome, treatment, covariates and (optionally) an instrument.

dml_data = dml.DoubleMLData(df, y_col='net_tfa', d_cols='e401', x_cols=X)

- No comments on this step yet — be the first.

Log in to comment on this step.

Choose ML learners for the nuisances

Data preparation — shapes the raw inputs into what the estimator expects.

e.g. random forest / lasso for E[Y|X] and E[D|X]; estimated by cross-fitting.

ml_l = RandomForestRegressor(); ml_m = RandomForestClassifier()

- No comments on this step yet — be the first.

Log in to comment on this step.

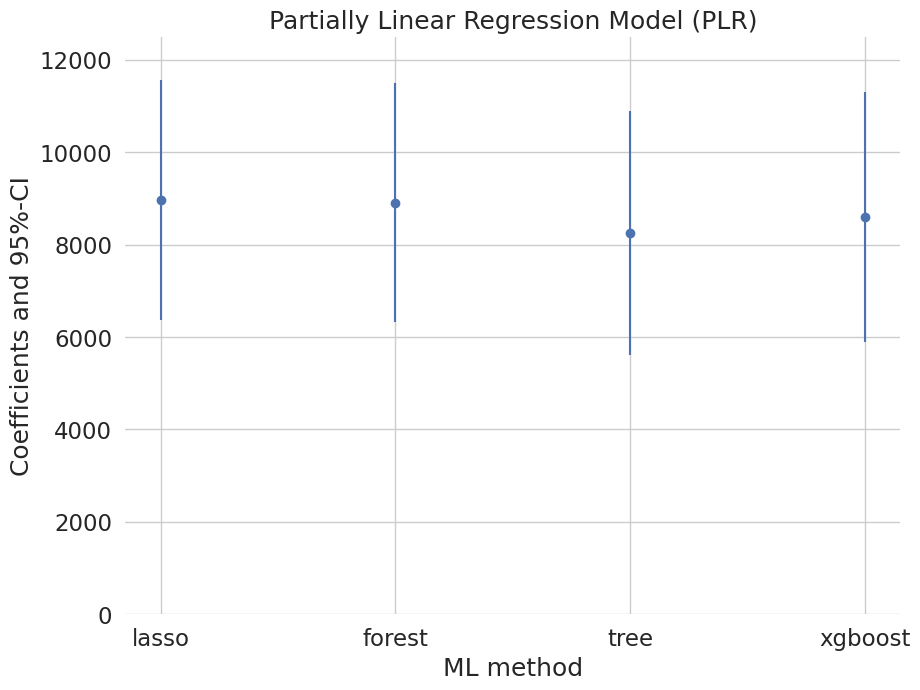

[DoubleML] Double/debiased ML — PLR / IRM / IIVM

The core estimate — where the causal quantity itself is computed.

Partially-linear regression (PLR) for the average effect, with orthogonal scores.

Double/debiased ML — PLR / IRM / IIVM — Neyman-orthogonal, cross-fitted estimation of treatment effects with arbitrary ML nuisance learners.

dml.DoubleMLPLR(dml_data, ml_l, ml_m).fit().summary

- No comments on this step yet — be the first.

Log in to comment on this step.

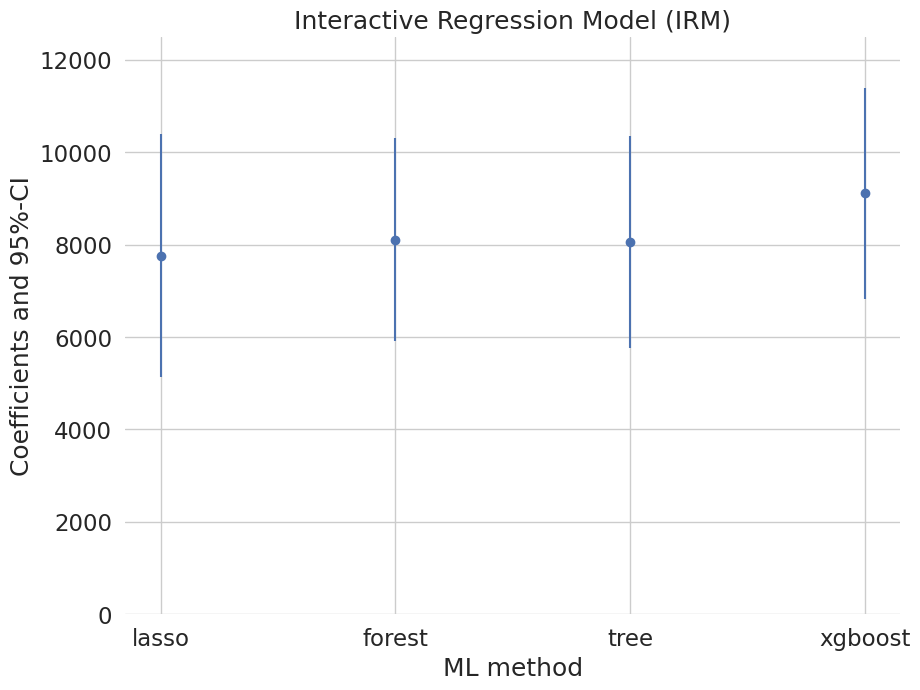

IRM / IIVM cross-checks

A robustness check — does the headline result survive a different lens?

Interactive (IRM) and IV (IIVM) models as alternative identifications.

dml.DoubleMLIRM(dml_data, ml_g, ml_m).fit()

- No comments on this step yet — be the first.

Log in to comment on this step.

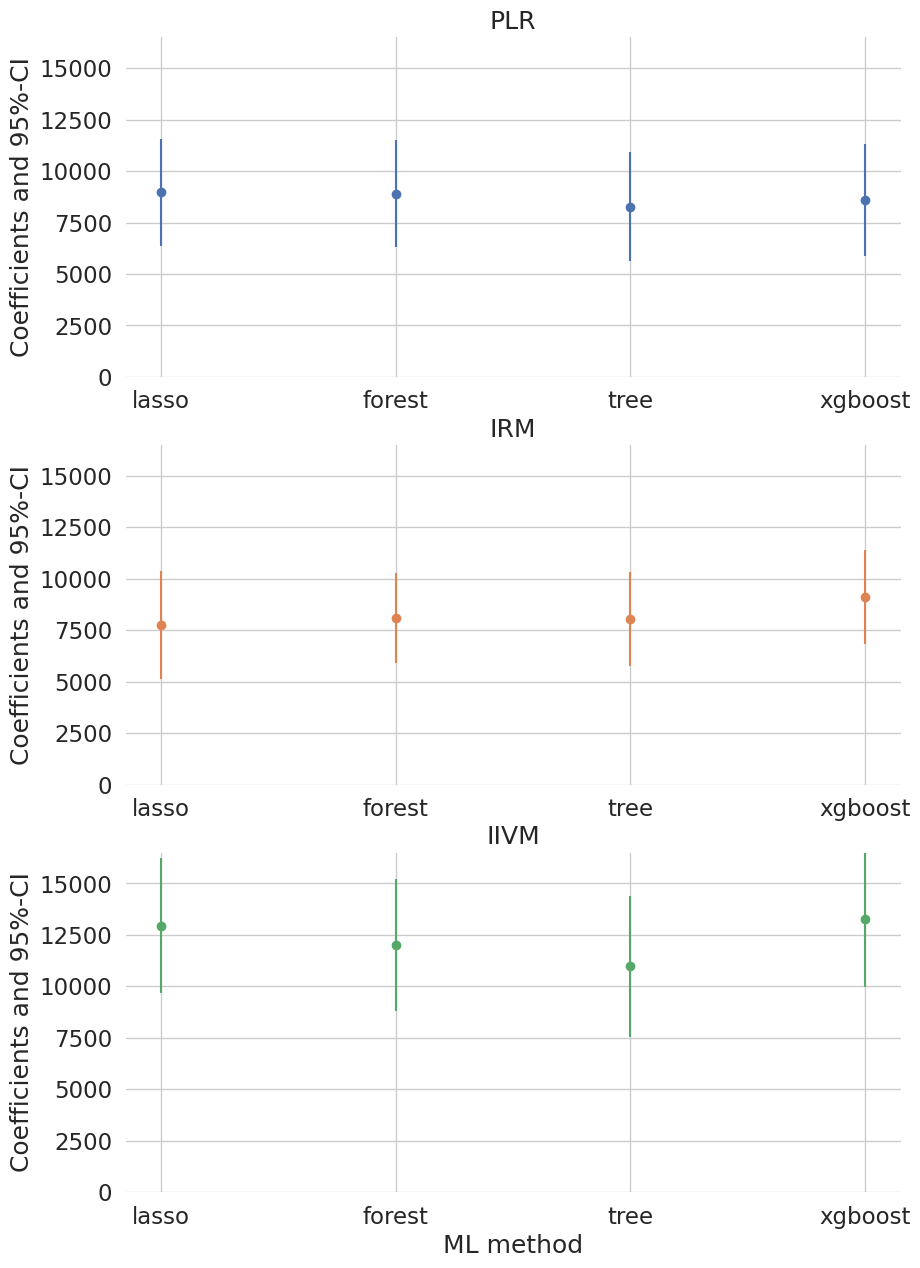

Coefficient comparison plot

Reporting — turn the numbers into a figure or table a reader can act on.

Compare estimates across PLR/IRM/IIVM × learners with 95% confidence intervals.

# error-bar plot of coef ± 1.96·se per model × learner

- No comments on this step yet — be the first.

Log in to comment on this step.

Output · what you get 4 figures

Figures reproduced from DoubleML — Bach, Chernozhukov, Kurz & Spindler — unofficial community showcase; all credit to the original authors.

The DoubleML 401(k) example (SIPP data). Build the DoubleMLData, choose ML learners, and estimate the effect three ways (PLR / IRM / IIVM). Unofficial summary.

Discussion (3)

Log in to join the discussion.

Cross-fitting + Neyman-orthogonal scores = you can throw any ML at the nuisances and still get √n-consistent, valid CIs. This is the way.

And it generalizes AIPW cleanly. PLR for a quick read, IRM when effects are nonlinear in X.

The 401(k) example is the perfect teaching case. Same data, three orthogonal scores, sane answers.

Pairs beautifully with GRF: DoubleML for the average, causal forest for the heterogeneity.